What is BIR60?

Salaries tax, also known as BIR60, is one of the income taxes in Hong Kong. It is levied on the annual income and allowances received by employees working in Hong Kong. Hong Kong employees are obliged to submit annual salaries tax to the Inland Revenue Department.

BIR60 calculation

Salary tax is calculated on the basis of the actual taxable income of the employee in the tax year at progressive tax rates; or on the net income at standard tax rates, whichever is the lower.

Actual taxable income = total income – total deductions – total allowance

Net Income = Total Income – Total Deductions

The tax year is from April 1st to March 31st of the following year. The annual provisional salaries tax is assessed on the basis of the previous year’s income minus deductions (and allowances).

What are the deductible items in BIR60?

Fortunately, there are many deductible items under Hong Kong salaries tax that can quickly reduce your taxable net income. Among these possible deductions are the following:

- Payments and disbursements (subject to conditions set by the Tax Office)

- Depreciation of plant, equipment and machinery used to generate revenue

- Any self-education expenses for career and knowledge advancement

- Make charitable contributions to approved programs and funds

- Qualifying Home Loan Interest

- Pension expenses

While there are several possible deductions that can reduce taxable net income, there are still many qualifications and necessary approvals that need to be obtained. It is important to understand any deductions you have so that you can apply them correctly when filing.

Notes on BIR60

It is vital that every taxpayer files an accurate tax return with the Inland Revenue Department (IRD) every year. After receiving the salary, the assessment time of Hong Kong salaries tax is from April 1 to the end of March of that year. Tax returns will be mailed by May 1 and should be filed within one month of the date they are issued to taxpayers.

An important note to remember is that even if a taxpayer did not bring in any income during the taxable period, they must still declare to the tax office the “0” income they receive on their tax forms. Married individuals can request a joint assessment or a single assessment, depending on their circumstances.

Employers must file their tax returns within three months of the date the tax office issued the refund. The owner will then receive a Notice of Assessment, which is a notice of the amount the company is responsible for paying payroll tax.

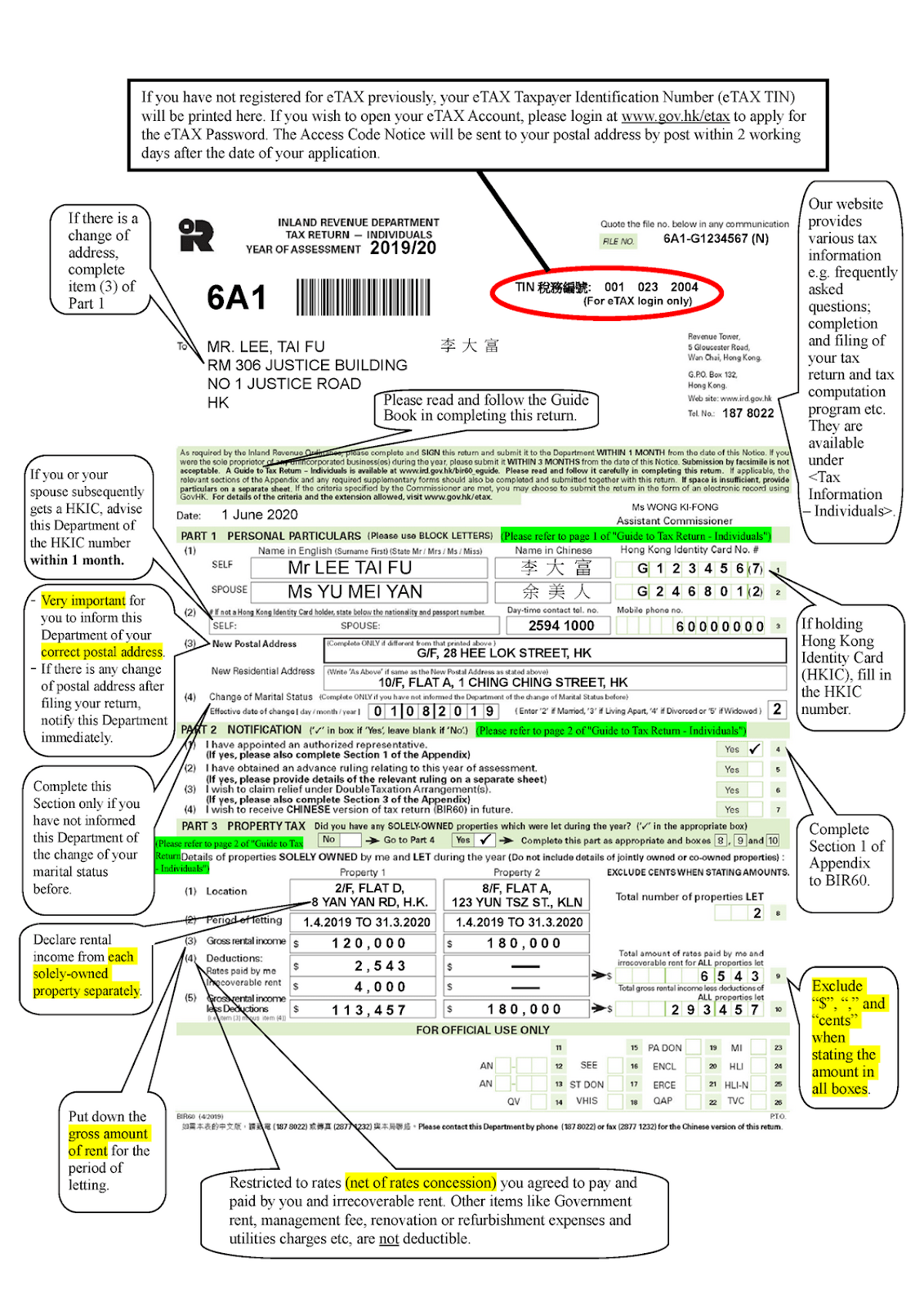

BIR60 sample

BIR60 form refers to this link.

As an employee, your obligation is primarily to inform the IRD of your payable salaries tax and any changes. IRD must also be notified when a new source of income is acquired or when any source of income is lost.

If the employer hires an employee who may be subject to salaries tax, he must also fill in an IR56E form within 3 months (or fill in the IR56E through the eTax).

Workstem

Best recommended! Workstem one-stop cloud calculation & human resources management platform includes a complete tax reporting function, not only helping you record employee entry dates, payroll data, payroll history records, MPF contribution records, etc., but also custom income increase/decrease, and put it under different taxation rules. When the tax filing season comes, Workstem will help you generate and export all employees’ tax return XML documents with one click, and upload them to the eTax platform easily, allowing you to get through tax season with ease!