If an employee leaves Hong Kong permanently or for a long time, the employer needs to:

- Know the employee’s exact expected date of departure

- File two IR56G forms (or by electronic means) to Inland Revenue Department (IRD) one month before the employee’s expected departure date

- From the date of filing the IR56G form by the employer, no remuneration (including salary, commission, bonus, and rent/expense reimbursement) can be paid to the employee until the employee completes the tax clearance procedure and shows receipt of the Letter of Release [IR607] issued by IRD to the employer.

Note: If the employer has already filed IR56G for the employee, there’s no need to file another IR56G at the end of the year. Filing two different IR56G forms for the same employee may result in repeated taxation.

Read More:

Tax Clearance – Things to be done / noted by Employer and Employee (IR6158)

You or your employee is going to leave Hong Kong – What are you required to do under the tax law?

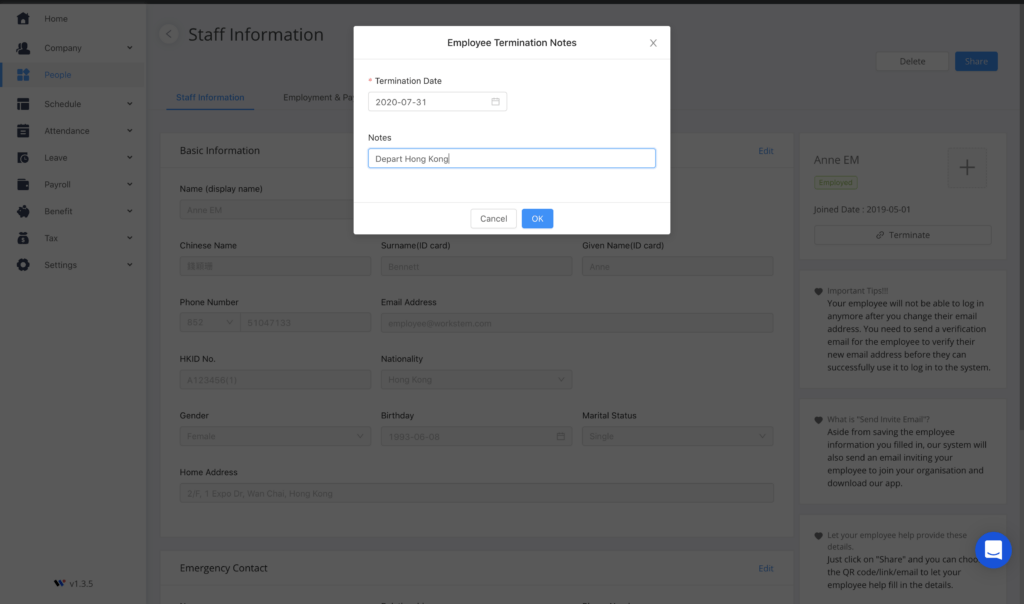

If employees resign because of further studies abroad or immigration, only after knowing clearly the employee’s estimated time of departure can the HR properly file the form to IRD.

When an employee resigns, our HRM System – Workstem can help you record his/her departure date, reason, and even detailed notes! IR56G can subsequently be exported with one click based on the information you filled in, no need to input it one by one!

![[418 Guide] Ordinance 418 And Continuous Contract](https://www.workstem.com/wp-content/uploads/2023/08/Untitled-design-min-350x220.png)